In bitcoin we trust?

Part 6: The politics of crypto and Web3's “adoption problem”

Hayek’s adoption problem

Among his numerous contributions Hayek is known for defending a desovereigntised or, in his own usage, “denationalised” monetary system where government issued currencies would be replaced by those issued by private banks.1 Particularly with respect to the money supply and the setting of interest rates, such a system, he argued, would help avoid the worst excesses of legacy monetary systems, where centralised decisions can have an adverse effect upon inflation and the economy’s ability to adjust to cyclical change.

Yet, the author of Law, Legislation, and Liberty also conceded that it was unlikely that his radical proposal would ever be adopted, so much so that by the 1980s he came to regard it as “completely utopian”. The primary obstacle in this respect was political, for the very agency that would be called upon to give up its control of the monetary system, either the central bank or, if this were not independent, the state itself, would also be entrusted with implementing the policy. “I don’t believe we shall ever have good money again before we take it out of the hands of government,” Hayek concluded in a 1984 interview given at the University of Freiburg in Germany:

Radical proposals such as his, then, would always face a serious “adoption problem.”

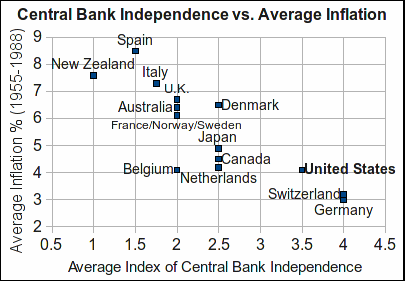

To be sure, there is a sense in which Hayek’s proposal is as politically premature as it is radical. After all, and before resorting to denationalisation, one can remove political control of monetary policy by simply making central banks independent of it. This, of course, is what Germany did with the Deutsche Bundesbank in 1951, so it is curious that Hayek did not consider this option, at least in this interview, and especially since the move toward central bank independence was well underway by the time he gave it. Indeed, subsequent research has shown that central bank independence correlates strongly with lower rates of inflation, precisely because it means that politicians have less discretion in manipulating the monetary environment for shorter-term political ends rather than in the longer-term general interest.2

Moreover, this correlation also calls into question not just the political hastiness of Hayek’s proposal, but the persuasiveness of the quasi-Public Choice critique of the state that underlies it. There is no obvious reason why policymakers could not make policy recommendations on the basis of this research, which politicians could, and in the case of Germany and other countries, clearly did accept, even though this meant relinquishing at least direct control of monetary policy. So, even in Hayek’s day the idea that the adoption problem was so grave as to make the monetary status quo unchallengeable was far-fetched.3

Of course, defenders of market competition in money could always argue that what may be true for central bank independence may not be true for denationalisation. As a more radical option, and even if central bank independence is politically “doable” in the way history has shown, it stands to reason that Hayekian denationalisation would face even greater political obstacles to its introduction, despite there being reason to believe that outcomes under such a system would be better than those under central bank independence (more on which in the final part of this essay).

But all of this notwithstanding, Hayek’s proposal merits attention, and not just because it seems uncannily prescient of desovereigntised monetary systems such as Bitcoin. In highlighting the political difficulty that the denationalisation of money would face, Hayek also hinted at a means of its resolution that seems equally far-sighted. Whilst “[w]e can’t take [money] violently out of the hands of government,’ he said, what ‘we can do is by some sly, roundabout way introduce something they can’t stop.”

It is here where for many in the Web3 community Hayek is a pioneer avant la lettre in a second sense, for the emergence of bitcoin appears to be not just the kind of desovereigntised monetary arrangement that the author of Law, Legislation and Liberty hoped for - more than thirty years before its emergence. Its emergence is also an example of precisely that “sly, roundabout” and unstoppable solution to the adoption problem, where the increasingly large stake that businesses and both institutional and retail investors have in the space’s success has begun to tell politically. Indeed, if one takes either market capitalisation (some £2tn at the time of writing), the number of US citizens who own or have owned cryptocurrency (some 145 million), or the record-breaking success of the launch of bitcoin exchange traded funds (ETFs) in January of this year as proxies, the economic clout of those invested in crypto appears set to keep growing until the political demand for acceptance, and suitable regulation, becomes impossible to ignore.4

Indeed, this market-driven “sly, roundabout” solution to the adoption problem is already underway. Governmental authorities in the United States are already beginning to add bitcoin to their balance sheets,5 and developments in the current US electoral cycle,6 including bipartisan support for pro-crypto measures in the United States Congress,7 historically unprecedented campaign contributions from the crypto industry,8 and proposals for bitcoin to be added to the US strategic reserve alongside gold, other precious metals, and foreign fiat currencies, further attest to this change.9 Finally, and irrespective of these developments, Web3 in any case presents a “genie out of the bottle problem” for the state, where advances in technology force its legislative and regulatory hand. In the case of bitcoin, and of Web3 more generally, denying that its emergence will eventually necessitate new regulatory systems and rules, and quite possibly new ways of thinking about those systems and rules, may come to be seen as about as far-sighted as denying the impact that twentieth century advances in avionics had upon the rules governing transport systems.

Thus, because it removes executive control of money from the hands of central authority, and represents a “sly, roundabout”, or “bottom-up”, means of effecting change - change as “spontaneous” rather than directed, as Hayek would say - bitcoin will see to it that Hayek’s vision of a denationalised monetary system, free from government control and conceived more than thirty years before its emergence, becomes a reality, and possibly sooner than many expect.

Bitcoin’s adoption problem

Yet, this flattering view of Hayek’s place in history is not that straightforward, for our discussion of centralised, decentralised, and radically decentralised governance structures in Part 2 also revealed an important difference between his idea of denationalisation and a cryptocurrency such as bitcoin.